The usual line on small-cap stocks is “higher risk, higher return.” They’re certainly proving that first part this year.

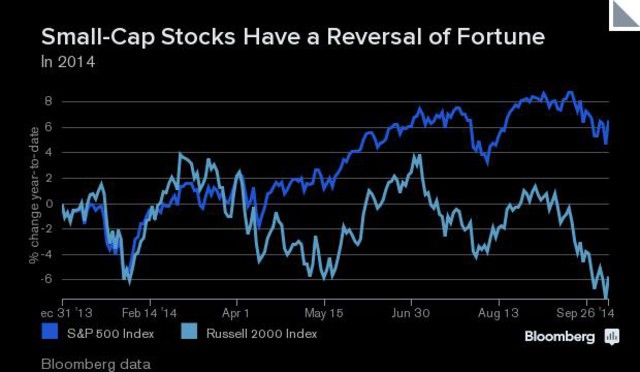

After a 2.7 percent drop yesterday, the small-cap Russell 2000 index is down 8.2 percent this year, while the large-cap S&P 500 Index is up 4.3 percent year-to-date. That’s after a 14-year run where small caps more than doubled the S&P 500’s return. That run was part of a long record. From 1926 to 2012, the smallest tenth of the market has beaten the largest tenth by almost four percentage points per year, Symmetry Partners estimates.

There’s just one thing. Most small-cap mutual fund investors don’t stay invested long enough to benefit from that performance edge. They treat small-cap stocks like fashion accessories. They move in and out of small caps as the markets rise and fall, rather than holding them to diversify their portfolios for the long term.

To treat small caps as a trend and then chase them like one is a sure way to hurt returns. Many investors buy and sell mutual funds at precisely the wrong times, resulting in returns that are worse than the performance of the funds they invest in. That happens most often in niche sector funds, like those that focus on small caps, Morningstar data show. Individual investors lagged the very sector funds they invested in by 3.1 percent per year over the last decade period. They only lagged 1.7 percent behind the performance of large-cap U.S. equity funds they bought.

Small caps have the appeal of a lottery: If the timing’s right, an investor can get very rich. Early investors in Keurig Green Mountain Inc. (GMCR), a $281 million company in 2006, have enjoyed growth of a company now worth $23.3 billion. To win like that, though, investors have to endure higher trading costs, day-to-day volatility and a greater number of blow-ups and bankruptcies than they would see with large-caps.

Patience also comes in handy. Despite their overall outperformance over the last 14 years, small caps lagged their bigger brethren from 1981 to 2000, long enough to shake the faith of any true believer.

And their rewards don’t take expenses into account. Vanguard’s small-cap exchange-traded fund has an expense ratio 80 percent higher than its S&P 500 ETF, and actively managed funds are similarly more expensive. Take into account these extra costs and adjust for risk, and small-cap stocks lose their edge over large caps, says Andy Rachleff, chairman of online adviser Wealthfront.

A better solution, he says, is the Vanguard Total Stock Market ETF (VTI). It includes stocks of all sizes for an expense ratio of 0.05, the same as Vanguard’s S&P 500 fund.

After a 2.7 percent drop yesterday, the small-cap Russell 2000 index is down 8.2 percent this year, while the large-cap S&P 500 Index is up 4.3 percent year-to-date. That’s after a 14-year run where small caps more than doubled the S&P 500’s return. That run was part of a long record. From 1926 to 2012, the smallest tenth of the market has beaten the largest tenth by almost four percentage points per year, Symmetry Partners estimates.

There’s just one thing. Most small-cap mutual fund investors don’t stay invested long enough to benefit from that performance edge. They treat small-cap stocks like fashion accessories. They move in and out of small caps as the markets rise and fall, rather than holding them to diversify their portfolios for the long term.

To treat small caps as a trend and then chase them like one is a sure way to hurt returns. Many investors buy and sell mutual funds at precisely the wrong times, resulting in returns that are worse than the performance of the funds they invest in. That happens most often in niche sector funds, like those that focus on small caps, Morningstar data show. Individual investors lagged the very sector funds they invested in by 3.1 percent per year over the last decade period. They only lagged 1.7 percent behind the performance of large-cap U.S. equity funds they bought.

Small caps have the appeal of a lottery: If the timing’s right, an investor can get very rich. Early investors in Keurig Green Mountain Inc. (GMCR), a $281 million company in 2006, have enjoyed growth of a company now worth $23.3 billion. To win like that, though, investors have to endure higher trading costs, day-to-day volatility and a greater number of blow-ups and bankruptcies than they would see with large-caps.

Patience also comes in handy. Despite their overall outperformance over the last 14 years, small caps lagged their bigger brethren from 1981 to 2000, long enough to shake the faith of any true believer.

And their rewards don’t take expenses into account. Vanguard’s small-cap exchange-traded fund has an expense ratio 80 percent higher than its S&P 500 ETF, and actively managed funds are similarly more expensive. Take into account these extra costs and adjust for risk, and small-cap stocks lose their edge over large caps, says Andy Rachleff, chairman of online adviser Wealthfront.

A better solution, he says, is the Vanguard Total Stock Market ETF (VTI). It includes stocks of all sizes for an expense ratio of 0.05, the same as Vanguard’s S&P 500 fund.

source: Bloomberg

RSS Feed

RSS Feed